Public Finance

Public finance, a branch of economics, examines the government’s role in the economy, specifically focusing on revenue and expenditure management. It assesses how governments raise funds, allocate resources, and impact the economy to achieve desired outcomes while avoiding undesirable consequences.

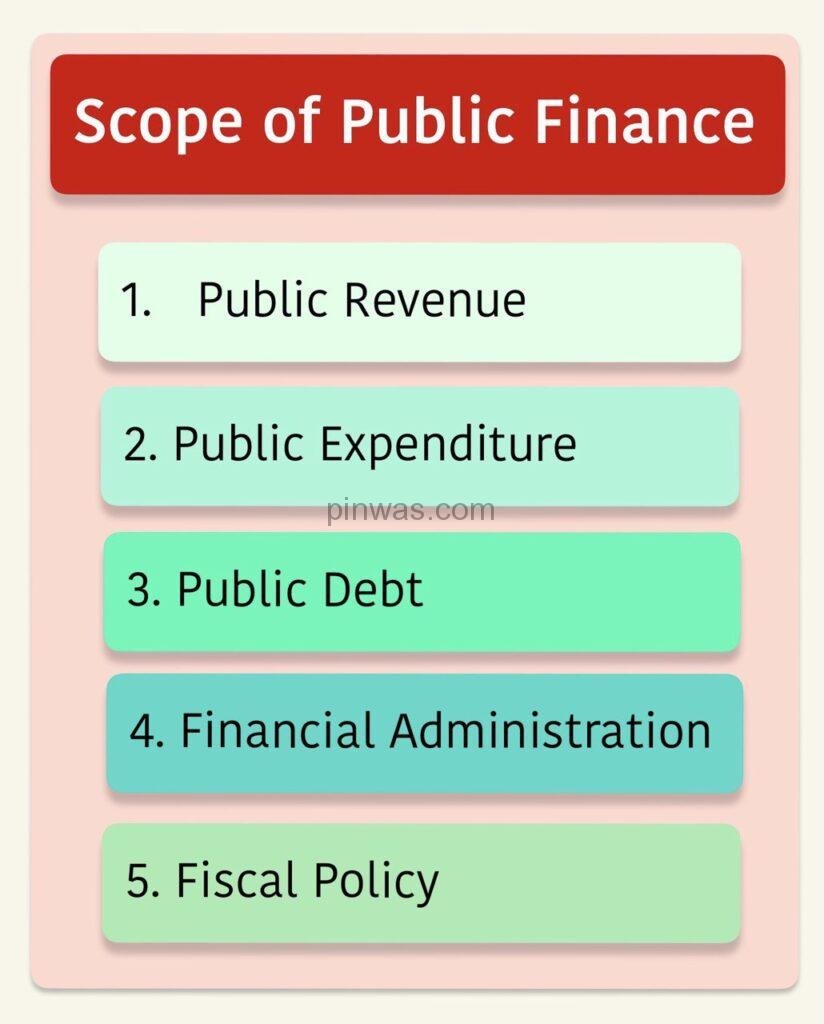

In contemporary times, the field of ‘Public Finance’ encompasses five major sub-categories, which are :

- Public Revenue : This area focuses on the means of generating public income, encompassing both tax and non-tax sources. It delves into the principles guiding taxation, tax rates, the impact of taxes on individuals and businesses, as well as how taxes may shift and their broader effects.

- Public Expenditure : This segment examines the fundamental principles governing government spending. It explores the consequences of public expenditure and methods for its control and management.

- Public Debt : Within this aspect, the methods of obtaining loans from both domestic and international sources are analysed. It includes the assessment of the burden, consequences, and strategies for redeeming public debt.

- Financial Administration : Financial administration entails the comprehensive study of various aspects related to the government budget. The budget serves as the annual master financial plan of the government. This sub-category encompasses setting objectives, steps in budget preparation, approval processes, allocation of funds, performance evaluation, and financial auditing.

- Fiscal Policy : Fiscal policy involves the use of tools such as taxes, subsidies, public debt management, and public expenditure as instruments to achieve economic goals and regulate the overall economy.

Fiscal Policy

Fiscal policy, one of the primary economic policies employed by governments alongside monetary policy, is the strategic use of government spending and taxation to shape the economy. It is pivotal in achieving overarching macroeconomic objectives, including full employment, price stability, and economic growth.

There exist two fundamental categories of fiscal policy :

- Expansionary Fiscal Policy : This approach seeks to invigorate the economy by either augmenting government spending or reducing taxes. Examples include investing in public infrastructure or providing tax incentives. It comes into play during recessions when the economy lags and unemployment is high.

- Contractionary Fiscal Policy : This strategy aims to moderate economic growth by either curtailing government spending or increasing taxes. Measures might encompass scaling back public programs or raising taxes on businesses and individuals. It’s typically deployed in times of high inflation when the economy surges too rapidly, causing prices to escalate.

Fiscal policy’s implementation involves both the legislature and the executive branch of government. The legislature enacts laws authorising government spending and taxation, while the executive branch executes these laws.

Examples of fiscal policy include :

Expansionary Fiscal Policy :

- Increased unemployment benefits and stimulus checks during the COVID-19 pandemic to support individuals and businesses.

- Increased government spending on infrastructure (e.g. roads and bridges) to stimulate the economy.

- Tax cuts for businesses to boost investment and hiring.

Contractionary Fiscal Policy :

- Raising taxes on individuals to reduce disposable income and curb consumer spending.

- Cutting spending on social welfare programs to decrease available funds for individuals.

- Raising taxes and reducing government spending in the early 1980s in the United States to combat inflation, although it resulted in a recession.

Public Finance and Fiscal policy : Relation

Public finance and fiscal policy are closely related but distinct concepts in government economics.

Public finance encompasses the study of government’s economic role, including revenue, spending, and policy impact.

Fiscal policy is a subset of public finance, focusing on how government uses spending and taxation to influence the economy.

Public finance sets the theoretical framework, while fiscal policy is its practical application.

Public finance covers various aspects of government finance, including taxation, spending, and borrowing.

Fiscal policy hones in on using government budgets for short-term goals like recession stimulus or inflation control.

Public finance addresses long-term economic concerns such as sustainable growth and income distribution.

| Base | Public Finance | Fiscal Policy |

| Scope | Broader | Narrower |

| Focus | Role of Govt. in the economy | Govt. use of spending & taxation to influence the economy |

| Example | Taxation, Govt. Expenditure, Govt. debt, Social Welfare Programmes, Public Investment. | Expansionary Fiscal policy, Contractionary Policy. |

Examples of public finance and fiscal policy :

Public finance :

- Analysing tax policies’ effects on economic efficiency and equity.

- Assessing government spending’s impact on growth and social welfare.

- Evaluating government debt sustainability.

Fiscal policy :

- Cutting taxes to stimulate the economy during a recession.

- Increasing infrastructure spending to boost economic growth.

- Raising taxes to combat inflation.

In summary, public finance provides the framework for understanding government budgeting and its economic impact, while fiscal policy is the tool governments use to achieve specific economic goals within this framework. Both concepts are crucial for comprehending the government’s role in the economy.

Public Finance and Fiscal Policy of UP

The public finance of Uttar Pradesh is the system by which the government of the state raises and spends money. The state’s revenue comes from a variety of sources, including taxes, fees, and grants from the central government. The state’s expenditure is on a variety of services, including education, healthcare, infrastructure, and social welfare.

The public finance of Uttar Pradesh has been under strain in recent years due to a number of factors, including the COVID-19 pandemic, the global economic slowdown, and the rising cost of living. In 2020-21, the state reported a revenue deficit of Rs 2,367 crore, the first in 14 years.

The state government has taken a number of steps to improve its fiscal position, including increasing taxes, reducing expenditure, and improving tax administration. However, more needs to be done to address the state’s financial challenges.

Here is a summary of the key trends in the public finance of Uttar Pradesh in recent years:

- Revenue receipts: The state’s revenue receipts have grown steadily in recent years, but the rate of growth has slowed down in recent years. The main sources of revenue receipts are taxes, fees, and grants from the central government.

- Revenue expenditure: The state’s revenue expenditure has also grown steadily in recent years, but the rate of growth has been higher than that of revenue receipts. This has led to a widening of the revenue deficit. The main components of revenue expenditure are salaries, pensions, and subsidies.

- Capital expenditure: The state’s capital expenditure has been relatively stagnant in recent years. This has led to a decline in the state’s infrastructure.

- Fiscal deficit: The state’s fiscal deficit has widened in recent years. This is due to the widening of the revenue deficit and the relatively stagnant capital expenditure.

- Debt: The state’s debt has also increased in recent years. However, the debt-to-GSDP ratio is still below the permissible limit of 35%.

The following are some of the challenges facing the public finance of Uttar Pradesh:

- Low tax-GDP ratio: The tax-GDP ratio of Uttar Pradesh is one of the lowest in India. This means that the state is not able to generate enough revenue to meet its expenditure needs.

- High dependence on central grants: Uttar Pradesh is one of the most dependent states on central grants. This means that the state is vulnerable to changes in the central government’s fiscal policy.

- High revenue deficit: The state has a high revenue deficit, which means that its revenue expenditure is higher than its revenue receipts. This is unsustainable in the long term.

- Rising debt: The state’s debt is rising, which increases the burden on future generations.

The following are some of the measures that the state government can take to improve its public finance:

- Increase the tax-GDP ratio: The state government can increase the tax-GDP ratio by improving tax administration, widening the tax base, and reducing tax exemptions.

- Reduce revenue expenditure: The state government can reduce revenue expenditure by rationalizing subsidies, improving efficiency in public spending, and reducing corruption.

- Increase capital expenditure: The state government can increase capital expenditure by mobilizing private investment and borrowing from the market.

- Improve fiscal discipline: The state government can improve fiscal discipline by setting realistic fiscal targets and adhering to them.

The public finance of Uttar Pradesh is important for the state’s economic development and social welfare. The state government needs to take steps to improve its fiscal position and address the challenges it faces.

Fiscal Responsibility & Budget Management Act, 2004

(Mid-term Fiscal Restructuring Policy, 2023)

Background

Every year, as per the Uttar Pradesh Fiscal Responsibility and Budget Management Act (FRBM) of 2004 (updated version), the state government of Uttar Pradesh must share a Mid-term Fiscal Restructuring Policy. This policy includes financial goals for the next five years, highlights of past achievements, spending details, and plans. The format for this policy is defined in the Uttar Pradesh Fiscal Responsibility and Budget Management Rules of 2006, and it’s presented alongside the annual budget to both houses of the State Legislature.

Objectives

The Uttar Pradesh Mid-term Fiscal Restructuring Policy for 2023 has been developed in accordance with the Act and Rules. It includes estimates for the budgets of 2022-23, revised estimates, and budget estimates for 2023-24, as well as projections for the following three years, namely 2024-25, 2025-26, and 2026-27, as outlined in Table :

- The objectives set for the fiscal years 2024-25, 2025-26, and 2026-27 are as follows:

- Gross State Domestic Product (GSDP) : Based on the new series with a base year of 2011-12, advance estimates have been made.

- Base Year : Estimates of receipts and expenditures for various items have been made based on the fiscal year 2023-24 (budget estimates) as the base year.

- State’s Own Tax Revenue : Annual growth rates of 13 percent for the fiscal year 2024-25 and 14 percent for the subsequent years have been estimated for GST and VAT.

- State’s Non-Tax Revenue : An annual growth rate of 6 percent for the fiscal year 2023-24 and subsequent years has been estimated.

- Share of Central Taxes : Calculations have been made for the state’s share in central taxes based on a growth rate of 13 percent for the fiscal year 2024-25 and 14 percent for subsequent years, starting from the budget estimates of 2023-24.

- Central Government Grants : A general increase of 10 percent has been applied to this item.

- Expenditure on Revenue : Expenditure on revenue, based on the revised estimate for the fiscal year 2022-23 and an annual increase of 11 percent for the fiscal year 2024-25 and 11.5 percent thereafter, has been calculated.

- Salaries : A 10 percent annual increase in expenditure on salaries for state employees and employees of state-funded organisations has been estimated.

- Pension : A 10 percent increase in pension expenditure has been assumed.

- Interest : The expenditure on interest, based on the average interest rate on state loans, is estimated at around 9 percent.

- Capital Expenditure : Based on the budget estimate for the fiscal year 2023-24, capital expenditure has been estimated with a general increase in subsequent years.

- Loans and Advances : Loan recovery and loans approved by the state government have both been estimated with an annual increase of 10 percent.

- Loan Repayment : Loan repayment has been estimated based on actual repayment obligations.

- Debt Burden : The total debt burden of the state, including the financial year 2022-23 (revised estimate) and 2023-24 (budget estimate), is approximately INR 15,573.84 crores and INR 17,939.00 crores, respectively, under the ‘Special Assistance Scheme for Capital Investment by States’ by the central government. Estimates for subsequent years under this scheme have also been considered.

- The objectives set for the fiscal years 2024-25, 2025-26, and 2026-27 are as follows:

State Finance | |||||||

| Sr. No. | Items | 2022-23 BE | 2022-23 RE | 2023-24 BE | For next 3 years | ||

| 2024-25 | 2025-26 | 2027-28 | |||||

| 1. | Revenue Receipts (2+3) | 499212.71 | 478816.53 | 570865 | 640373.74 | 723811.27 | 818627.59 |

| 2. | Tax Revenue (a + b ) | 367153.76 | 354983.28 | 445871.59 | 503834.90 | 574371.78 | 654783.83 |

| (a) | State own revenue | 220655.00 | 185237.98 | 262634.00 | 296776.42 | 338325.12 | 385690.64 |

| (b) | State’s share in Centre taxes | 146498.76 | 169745.30 | 183237.59 | 207058.48 | 236046.66 | 269093.20 |

| 3. | Non-tax Revenue (c + d) | 132058.95 | 123833.25 | 124994.07 | 136541.85 | 149439.48 | 163843.76 |

| (c) | State’s own non-tax revenue | 23406.48 | 12294.74 | 23790.22 | 25218.22 | 26983.49 | 29142.17 |

| (d) | Grants in Aid from Centre | 108652.47 | 111538.51 | 101203.30 | 111323.63 | 122455.99 | 134701.59 |

| 4. | Capita Receipts (5 + 6) | 91739.00 | 97312.84 | 112427.08 | 122669.79 | 133936.77 | 146330.44 |

| 5. | Borrowings and Advances | 2565.00 | 2565.00 | 3312.18 | 3643.40 | 40007.74 | 4408.51 |

| 6. | Public borrowings | 89174.00 | 94747.84 | 109114.90 | 119026.39 | 129929.03 | 141921.93 |

| (e) | State’s internal borrowings | 86674.00 | 76674.00 | 88175.90 | 95993.49 | 104592.84 | 114052.12 |

| (f) | External Assistance for Projects (Bank to Bank) | 2500.00 | 18073.84 | 20939.00 | 23032.90 | 25332.19 | 27869.81 |

| 7. | Total Receipts (1 + 4) | 590951.71 | 576129.37 | 683292.74 | 763046.53 | 857748.03 | 964958.04 |

| 8. | Revenue Expenditure In which | 456089.06 | 424909.27 | 502354.01 | 557612.95 | 621738.44 | 696347.05 |

| 9. | Interest payments | 45987.46 | 45765.50 | 50255.56 | 54778.56 | 59708.63 | 65082.41 |

| 10. | Salaries | 79407.27 | 67543.31 | 86439.07 | 95082.98 | 104591.27 | 115050.40 |

| 11. | Salary assistant grant | 74162.39 | 62378.04 | 79722.13 | 87694.34 | 96463.78 | 106110.16 |

| 12. | Pension | 77077.75 | 59577.31 | 82422.38 | 90664.62 | 99731.08 | 109704.19 |

| 13. | Assistance to local bodies | 18008.70 | 18008.70 | 23719.62 | 26091.58 | 28700.74 | 31570.81 |

| 14. | Subsidy | 23209.05 | 25926.16 | 26364.80 | 29001.28 | 31901.41 | 35091.55 |

| 15. | General Assistance Grant (Non-Salary) | 566221.43 | 60643.65 | 63322.45 | 69654.70 | 76620.16 | 84282.18 |

| 16. | Grants for Capital Assets creation | 20148.41 | 21047.41 | 20851.31 | 22936.44 | 25230.09 | 27753.09 |

| 17. | Capital Expenditure In which | 159429.92 | 160363.02 | 187888.42 | 207779.85 | 231615.48 | 260291.70 |

| 18. | Capital Expenditure | 123919.85 | 126601.11 | 147492.29 | 165191.36 | 186666.24 | 212799.52 |

| 19. | Loan Repayments | 32563.29 | 22565.13 | 31118.43 | 32452.32 | 33799.45 | 35227.42 |

| 20. | Borrowings and Advances | 2946.78 | 11196.78 | 9214.70 | 10136.17 | 11149.79 | 12264.77 |

| 21. | Total Expenditure (8 + 17) | 615518.98 | 585272.29 | 690242.43 | 765392.80 | 853353.92 | 956638.76 |

| 22. | Revenue Savings | 43123.65 | 53907.26 | 68511.65 | 82763.79 | 102072.83 | 122280.54 |

| 23. | Fiscal deficit | 81177.98 | 81325.63 | 84883.16 | 88920.35 | 91735.47 | 98375.23 |

| 24. | Primary deficit | 35190.52 | 35560.13 | 34627.60 | 34141.78 | 32026.83 | 33292.82 |

| 25. | Debt burden | 666153.39 | 700445.52 | 784113.65 | 873034.00 | 964769.46 | 1063144.6 |

Fiscal Overview

Revenue Expenditure : The revised estimate for revenue expenditure for the fiscal year 2022-23 is INR 4,24,909.27 crores, and it is estimated to increase to INR 5,02,354.01 crores in the budget estimate for 2023-24.

Capital Expenditure : The revised estimate for capital expenditure for the fiscal year 2022-23 is INR 1,26,601.11 crores, which is estimated to increase to INR 1,47,492.29 crores in the fiscal year 2023-24 budget estimate.

Revenue Deficit : The goal of eliminating revenue deficit was achieved by the financial year 2006-07, and the state has maintained a surplus in revenue (surplus) since then, although due to the extraordinary economic conditions arising from the COVID-19 pandemic in the financial year 2020-21, there has been a revenue deficit situation.

Fiscal Policy Details

Revenue Department, Excise Department, Transport Department, Registration Department, and Geology and Mining Department are the main departments responsible for revenue generation in Uttar Pradesh. Various measures have been taken by these departments for resource growth from a revenue perspective.

Commerce Tax

The Special Rate Scheme for manufacturers of bricks and tiles has been effective since April 1, 2022, resulting in an estimated additional revenue of ₹300 crore. E-invoicing for taxpayers with an annual turnover exceeding ₹20 crore has also been implemented since April 1, 2022.

A centralised Command Center has been established for the monitoring of the Vehicle Tracking System on active fleet vehicles.

Under the GST, various government departments are registering and depositing due TDS (Tax Deducted at Source) with details to authorised officers.

Regular monitoring of payments exceeding ₹5 crore for projects is being carried out in terms of TDS deduction.

Regular reviews are being conducted for the resolution of pending VAT appeals by first appellate authorities.

Transport

A regular special checking campaign is being conducted against vehicles operating with outstanding dues, resulting in increased revenue collection.

Owners of vehicles residing in arrears are regularly sent demand letters, and if the dues are not paid, recovery notices are issued as per land revenue regulations.

Special checking campaigns are also being conducted against unauthorised operation of passenger vehicles and overloading of goods vehicles, with the collection of penalties through enforcement actions.

Stamps and Registration

In most districts of the state, the revaluation of the valuation list for the past 5 years had not been carried out, which was undertaken in the year 2022-23.

The system for online refund of unused stamps and unused online e-fees has been strengthened, leading to increased utilisation of this facility by stakeholders.

Excise Department

The excise policy for the financial year 2022-23 has been determined.

There has been an increase in processing fees for country liquor, renewal fees for licensed shops, and MGQ (Maximum Guaranteed Quantity), among others.

There has been an increase in processing fees for model shops and renewal fees for licensed shops.

The processing fees for beer and renewal fees for licensed shops have been increased.

Geology and Mining

Based on satellite images of important districts, mineral mapping of new mining areas for riverbed sand and morung (मोरंग) is being carried out by the respective districts.

To effectively control illegal mining/transportation, the department has developed an Integrated Mineral Surveillance System (IMSS) on the Mine & Mitra portal (www.minemitra.up.gov.in), utilising information and technology.

In addition to automated check gates, the department has developed a mobile app called “M-check” for the verification of transportation documents on other routes. Departmental officers are provided with RFID Hand Held Readers with the “M-check” app to facilitate the legal verification of mineral vehicles.

The system for depositing exchange fees from brick kilns online has been implemented on the departmental portal www.upmines.upsdc.gov.in, resulting in brick kiln owners in remote areas also being able to deposit regulatory fees.

The rate of imposed regulatory fees on vehicles carrying minor minerals from other states into the state has been increased by ₹50/- per cubic meter through a government order dated 10.08.2022, which is expected to increase revenue.

Fiscal Situation Analysis

The assessment of the fiscal situation can be based on several indicators as a percentage of the total state domestic product, some of the key indicators are listed in the table below —

Indicators as a percentage of Gross State Domestic Product (GSDP) | ||||||

| Items | 2022-23 BE | 2022-23 RE | 2023-24 BE | For next 3 years | ||

| 2024-25 | 2025-26 | 2026-27 | ||||

| 1. State’s own Tax Revenue | 10.8 | 9.0 | 10.8 | 10.8 | 10.9 | 11.0 |

| 2. State’s own Non-Tax Revenue | 1.1 | 0.6 | 1.0 | 0.9 | 0.9 | 0.8 |

| 3. Revenue Surplus | 2.1 | 2.6 | 2.8 | 3.0 | 3.3 | 3.5 |

| 4. Fiscal Deficit | 3.96 | 3.97 | 3.48 | 3.24 | 2.95 | 2.80 |

| 5. Total Borrowing & Order Liabilities | 32.5 | 34.2 | 32.1 | 31.7 | 31.0 | 30.2 |

The estimated share of own tax revenue as a percentage of the Gross State Domestic Product (GSDP) in the budget for the fiscal year 2022-23 is projected to be 10.8%, which is 90% higher than the revised estimate of ₹0.30 lakh crore. It is expected to further increase to 10.8% in the year 2023-24, and there is an expectation of continuous growth in the following years.

The state’s tax-to-GSDP ratio in the revised estimates for the fiscal year 2022-23 is 0.6%, which is projected to increase to 1.0% in the year 2023-24.

The budget estimates for the fiscal year 2022-23 had projected a fiscal deficit as a percentage of GSDP at 3.96, which is estimated to be 3.97% in the revised estimates. In the budget estimates for the year 2023-24, the fiscal deficit, as a percentage of GSDP, is estimated at 3.48%. It is projected to remain within the defined ratio as per the Fiscal Responsibility and Budget Management (FRBM) Act for the fiscal years 2024-25 and 2025-26. The limit is not yet determined for the fiscal year 2026-27 under the FRBM Act.

Sustainability of Fiscal Situation

For the assessment of fiscal sustainability, various other indicators are presented in Table.

Other important financial indicators | ||||||

| Items | 2022-23 BE | 2022-23 RE | 2023-24 BE | For next 3 years | ||

| 2024-25 | 2025-26 | 2026-27 | ||||

| 1. Salary + Pension + Interest / Revenue Receipts | 55.4% | 49.1% | 52.3% | 51.3% | 49.8% | 48.4% |

| 2. Salary + Pension + Interest / Revenue Expenditure | 60.7% | 55.54% | 59.5 | 58.9% | 58.0% | 56.9% |

| 3. Debt Service / Revenue Receipts | 13.7% | 14.3% | 12.5% | 12.1% | 11.5% | 11.0% |

| 4. Capital Expenditure / Fiscal Deficit | 152.7% | 155.7% | 173.8% | 185.8% | 203.5% | 216.3% |

| 5. Revenue savings / Revenue Receipts | 8.6% | 11.3% | 12.0% | 12.9% | 14.1% | 14.9% |

In the fiscal year 2023-24, it is estimated that revenue receipts will constitute 52.3% of the revenue expenditure, and revenue expenditure will be 59.5% of the total state domestic product (GSDP). It is expected that these ratios will decrease to 48.4% and 56.9% respectively by the year 2026-27.

The expenditure on debt servicing is projected to remain at 12.5% of revenue receipts in the fiscal year 2023-24, decreasing to 11.0% by the year 2026-27.

The Capital Outlay/Fiscal Deficit ratio signifies how much of the government’s net borrowing is being used for investment and asset creation. When this indicator is above 100%, it indicates that not only is 100% of the government’s net borrowing being used for capital expenditure but also a significant portion of it is being financed through revenue savings. In the budget for the year 2023-24, it is estimated that this ratio will be 173.8%, and continuous growth is expected in the following years.

In this way, all these indicators reflect the sustainability and strengthening of the fiscal situation. It also indicates that there are positive improvements in the quality of public spending.

Government Debt

In the budget estimates for the fiscal year 2022-23, the state’s government debt was calculated at ₹6,66,153.39 crores. In the corresponding revised estimates, it stands at ₹7,00,445.52 crores. It is estimated to further increase to ₹7,84,113.65 crores in the year 2023-24, which is 32.1% of the GSDP.

Investment in UP : Issues and Impact

Main Features of State Budgets